Page 185 - GSTL_16th July 2020_Vol. 38_Part 3

P. 185

2020 ] IN RE : SAFSET AGENCIES PVT. LTD. 423

7. There are different practices prevailing in the trade as to classifica-

tion, valuation and applicable GST rates on goods dealt in by the appellant.

Appellant had filed an application before the AAR seeking a ruling on

classification, valuation and applicable GST rates on goods dealt by the Appel-

lant. The purpose of appellant going for advance ruling was to have absolute

clarity as to its tax obligation.

Appellant sought advance ruling in respect of determination of classifi-

cation, valuation and GST rates applicable to various goods dealt with by it.

8. AAR admitted the appellant’s application in preliminary hearing

held on 28-11-2018.

9. AAR passed Order No. GST-ARA-86/2018-19/B-7 on 15-1-2019

specifying the classification, valuation and applicable GST rates on goods dealt

by the Appellant.

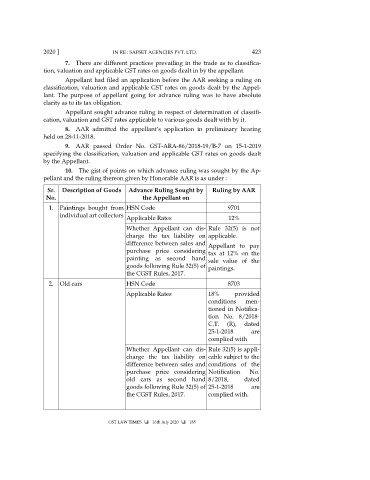

10. The gist of points on which advance ruling was sought by the Ap-

pellant and the ruling thereon given by Honorable AAR is as under :

Sr. Description of Goods Advance Ruling Sought by Ruling by AAR

No. the Appellant on

1. Paintings bought from HSN Code 9701

individual art collectors Applicable Rates 12%

Whether Appellant can dis- Rule 32(5) is not

charge the tax liability on applicable.

difference between sales and Appellant to pay

purchase price considering tax at 12% on the

painting as second hand sale value of the

goods following Rule 32(5) of paintings.

the CGST Rules, 2017.

2. Old cars HSN Code 8703

Applicable Rates 18% provided

conditions men-

tioned in Notifica-

tion No. 8/2018-

C.T. (R), dated

25-1-2018 are

complied with

Whether Appellant can dis- Rule 32(5) is appli-

charge the tax liability on cable subject to the

difference between sales and conditions of the

purchase price considering Notification No.

old cars as second hand 8/2018, dated

goods following Rule 32(5) of 25-1-2018 are

the CGST Rules, 2017. complied with.

GST LAW TIMES 16th July 2020 185