Page 93 - GSTL_16th July 2020_Vol. 38_Part 3

P. 93

2020 ] IN RE : SARDA BIO POLYMERS PVT. LTD. 331

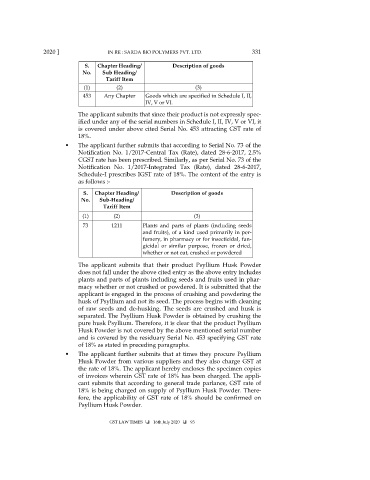

S. Chapter Heading/ Description of goods

No. Sub Heading/

Tariff Item

(1) (2) (3)

453 Any Chapter Goods which are specified in Schedule I, II,

IV, V or VI.

The applicant submits that since their product is not expressly spec-

ified under any of the serial numbers in Schedule I, II, IV, V or VI, it

is covered under above cited Serial No. 453 attracting GST rate of

18%.

• The applicant further submits that according to Serial No. 73 of the

Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017, 2.5%

CGST rate has been prescribed. Similarly, as per Serial No. 73 of the

Notification No. 1/2017-Integrated Tax (Rate), dated 28-6-2017,

Schedule-I prescribes IGST rate of 18%. The content of the entry is

as follows :-

S. Chapter Heading/ Description of goods

No. Sub-Heading/

Tariff Item

(1) (2) (3)

73 1211 Plants and parts of plants (including seeds

and fruits), of a kind used primarily in per-

fumery, in pharmacy or for insecticidal, fun-

gicidal or similar purpose, frozen or dried,

whether or not cut, crushed or powdered

The applicant submits that their product Psyllium Husk Powder

does not fall under the above cited entry as the above entry includes

plants and parts of plants including seeds and fruits used in phar-

macy whether or not crushed or powdered. It is submitted that the

applicant is engaged in the process of crushing and powdering the

husk of Psyllium and not its seed. The process begins with cleaning

of raw seeds and de-husking. The seeds are crushed and husk is

separated. The Psyllium Husk Powder is obtained by crushing the

pure husk Psyllium. Therefore, it is clear that the product Psyllium

Husk Powder is not covered by the above mentioned serial number

and is covered by the residuary Serial No. 453 specifying GST rate

of 18% as stated in preceding paragraphs.

• The applicant further submits that at times they procure Psyllium

Husk Powder from various suppliers and they also charge GST at

the rate of 18%. The applicant hereby encloses the specimen copies

of invoices wherein GST rate of 18% has been charged. The appli-

cant submits that according to general trade parlance, GST rate of

18% is being charged on supply of Psyllium Husk Powder. There-

fore, the applicability of GST rate of 18% should be confirmed on

Psyllium Husk Powder.

GST LAW TIMES 16th July 2020 93