Page 143 - GSTL_13th August 2020_Vol 39_Part 2

P. 143

2020 ] IN RE : HAZARI BAGH BUILDERS PVT. LTD. 229

cial use, entrusted to it by the Central Government for the purpose

of generating revenue by non-tariff measures.

We observe that in background of its function, especially of generat-

ing revenue, RLDA is leasing the parcels of land and thus it is a

rental or leasing service of land for commercial function. In a way, it

is clear from facts that RLDA is supplying rental or leasing service

involving own land. The said service is classifiable under HSN 9972

12 ‘rental or leasing services involving own or leased non-residential prop-

erty’.

Further, the Services of HSN 9972 12 falls under Serial No. 16(iii) of

the Notification 11/2017-Central Tax (Rate), dated 28-6-2017 (as

amended) and attracts GST @ 18% (SGST 9% + CGST 9%). The rele-

vant extract of the said Notification is as under -

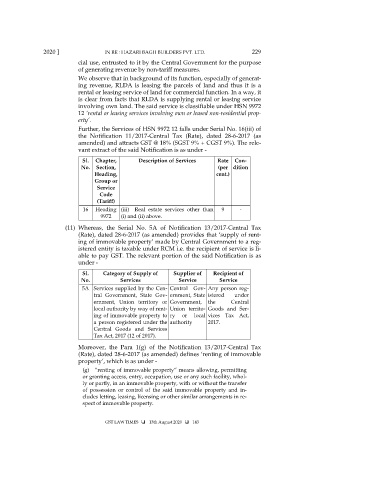

Sl. Chapter, Description of Services Rate Con-

No. Section, (per dition

Heading, cent.)

Group or

Service

Code

(Tariff)

16 Heading (iii) Real estate services other than 9 -

9972 (i) and (ii) above.

(11) Whereas, the Serial No. 5A of Notification 13/2017-Central Tax

(Rate), dated 28-6-2017 (as amended) provides that ‘supply of rent-

ing of immovable property’ made by Central Government to a reg-

istered entity is taxable under RCM i.e. the recipient of service is li-

able to pay GST. The relevant portion of the said Notification is as

under -

Sl. Category of Supply of Supplier of Recipient of

No. Services Service Service

5A Services supplied by the Cen- Central Gov- Any person reg-

tral Government, State Gov- ernment, State istered under

ernment, Union territory or Government, the Central

local authority by way of rent- Union territo- Goods and Ser-

ing of immovable property to ry or local vices Tax Act,

a person registered under the authority 2017.

Central Goods and Services

Tax Act, 2017 (12 of 2017).

Moreover, the Para 1(g) of the Notification 13/2017-Central Tax

(Rate), dated 28-6-2017 (as amended) defines ‘renting of immovable

property’, which is as under -

(g) “renting of immovable property” means allowing, permitting

or granting access, entry, occupation, use or any such facility, whol-

ly or partly, in an immovable property, with or without the transfer

of possession or control of the said immovable property and in-

cludes letting, leasing, licensing or other similar arrangements in re-

spect of immovable property.

GST LAW TIMES 13th August 2020 143