Page 144 - GSTL_13th August 2020_Vol 39_Part 2

P. 144

230 GST LAW TIMES [ Vol. 39

We observe that, RLDA being the statutory authority of Govern-

ment of India is providing services by way of renting of immovable

property to a registered person (i.e. the applicant), and renting of

immovable property includes leasing also, therefore the said ser-

vices are falling under the purview of Reverse Charge Mechanism.

The applicant being the recipient of service of leasing or renting of

immovable property is liable to pay GST under RCM.

(12) Whereas, to determine the rate of GST on supply made by RLDA to

the applicant, we have to go through the above discussed Para 10

and 11 together i.e. Chapter Heading 9972 of Notification 11/2017-

Central Tax (Rate), dated 28-6-2017 (as amended) with the Notifica-

tion No. 13/2017-Central Tax (Rate), dated 28-6-2017 (as amended).

Thus, we find that, the leasing services supplied by the RLDA to the

applicant falls under HSN 9972 12 attracting GST @ 18% (SGST 9%

+ CGST 9%).

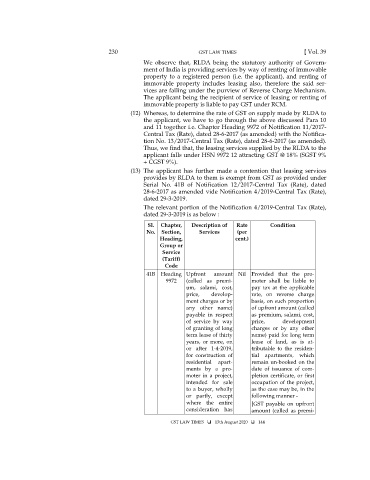

(13) The applicant has further made a contention that leasing services

provides by RLDA to them is exempt from GST as provided under

Serial No. 41B of Notification 12/2017-Central Tax (Rate), dated

28-6-2017 as amended vide Notification 4/2019-Central Tax (Rate),

dated 29-3-2019.

The relevant portion of the Notification 4/2019-Central Tax (Rate),

dated 29-3-2019 is as below :

Sl. Chapter, Description of Rate Condition

No. Section, Services (per

Heading, cent.)

Group or

Service

(Tariff)

Code

41B Heading Upfront amount Nil Provided that the pro-

9972 (called as premi- moter shall be liable to

um, salami, cost, pay tax at the applicable

price, develop- rate, on reverse charge

ment charges or by basis, on such proportion

any other name) of upfront amount (called

payable in respect as premium, salami, cost,

of service by way price, development

of granting of long charges or by any other

term lease of thirty name) paid for long term

years, or more, on lease of land, as is at-

or after 1-4-2019, tributable to the residen-

for construction of tial apartments, which

residential apart- remain un-booked on the

ments by a pro- date of issuance of com-

moter in a project, pletion certificate, or first

intended for sale occupation of the project,

to a buyer, wholly as the case may be, in the

or partly, except following manner -

where the entire [GST payable on upfront

consideration has amount (called as premi-

GST LAW TIMES 13th August 2020 144