Page 203 - GSTL_3rd September 2020_Vol 40_Part 1

P. 203

2020 ] IN RE : NAVNEETH KUMAR TALLA 137

20. From the above, it is clear that Sl. No. 7(v) now only covers supply

at functions which are occasional and event based. The supply of food to institu-

tions which were earlier covered under entry at Sl. No. 7(v) has been included

under Sl. No. 7(i). In the instant case the applicant is making supply of services in

the dining space of the hospitals which is squarely covered in the Explanation 1

to Sl. No. 7(i) and thereupon is liable to tax at the rate of 5% subject to the condi-

tion that credit of input tax charged on goods and services used in supplying the

services has not been taken.

21. Further, the above Notification No. 13/2018-State Tax (Rate), issued

in G.O.Ms No. 171, Revenue (CT-II) Department, dated 20-8-2018 was slightly

amended vide Notification No. 27/2018 as under :

In the said notification, -

(i) in the Table, -

(b) against serial number 7, in column (3), in item (i), in Explana-

tion 1, the words “school, college” shall be omitted;

However, Notification No. 11/2017-State Tax (Rate), issued in G.O.Ms No. 110,

Revenue (CT-II) Department, dated 29-6-2017 was totally revamped as per the

37th GST Council Meeting held on 20-9-2019 and Notification No. 20/2019-C.T.

(Rate), dated 30-9-2019, was issued which is as under :-

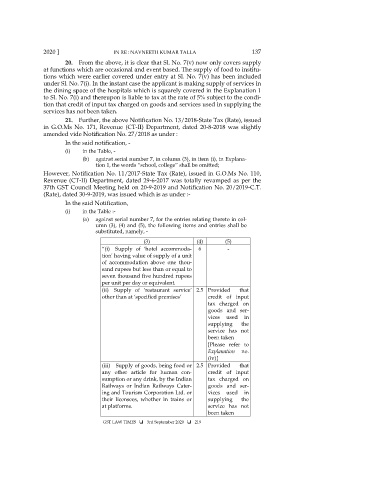

In the said Notification,

(i) in the Table :-

(a) against serial number 7, for the entries relating thereto in col-

umn (3), (4) and (5), the following items and entries shall be

substituted, namely, -

(3) (4) (5)

“(i) Supply of ‘hotel accommoda- 6 -

tion' having value of supply of a unit

of accommodation above one thou-

sand rupees but less than or equal to

seven thousand five hundred rupees

per unit per day or equivalent.

(ii) Supply of ‘restaurant service’ 2.5 Provided that

other than at ‘specified premises’ credit of input

tax charged on

goods and ser-

vices used in

supplying the

service has not

been taken

[Please refer to

Explanation no.

(iv)]

(iii) Supply of goods, being food or 2.5 Provided that

any other article for human con- credit of input

sumption or any drink, by the Indian tax charged on

Railways or Indian Railways Cater- goods and ser-

ing and Tourism Corporation Ltd. or vices used in

their licensees, whether in trains or supplying the

at platforms. service has not

been taken

GST LAW TIMES 3rd September 2020 219