Page 204 - GSTL_3rd September 2020_Vol 40_Part 1

P. 204

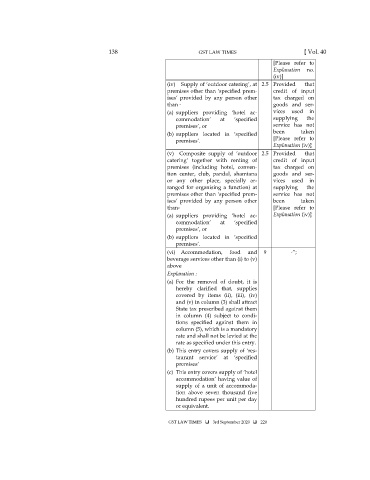

138 GST LAW TIMES [ Vol. 40

[Please refer to

Explanation no.

(iv)]

(iv) Supply of ‘outdoor catering’, at 2.5 Provided that

premises other than ‘specified prem- credit of input

ises’ provided by any person other tax charged on

than - goods and ser-

(a) suppliers providing ‘hotel ac- vices used in

commodation’ at ‘specified supplying the

premises’, or service has not

(b) suppliers located in ‘specified been taken

premises’. [Please refer to

Explanation (iv)]

(v) Composite supply of ‘outdoor 2.5 Provided that

catering’ together with renting of credit of input

premises (including hotel, conven- tax charged on

tion center, club, pandal, shamiana goods and ser-

or any other place, specially ar- vices used in

ranged for organising a function) at supplying the

premises other than ‘specified prem- service has not

ises’ provided by any person other been taken

than- [Please refer to

(a) suppliers providing ‘hotel ac- Explanation (iv)]

commodation’ at ‘specified

premises’, or

(b) suppliers located in ‘specified

premises’.

(vi) Accommodation, food and 9 -”;

beverage services other than (i) to (v)

above

Explanation :

(a) For the removal of doubt, it is

hereby clarified that, supplies

covered by items (ii), (iii), (iv)

and (v) in column (3) shall attract

State tax prescribed against them

in column (4) subject to condi-

tions specified against them in

column (5), which is a mandatory

rate and shall not be levied at the

rate as specified under this entry.

(b) This entry covers supply of ‘res-

taurant service’ at ‘specified

premises’

(c) This entry covers supply of ‘hotel

accommodation’ having value of

supply of a unit of accommoda-

tion above seven thousand five

hundred rupees per unit per day

or equivalent.

GST LAW TIMES 3rd September 2020 220