Page 249 - ELT_2nd_15th April 2020_Vol 372_Part

P. 249

2020 ] PEE CEE COSMA SOPE LTD. v. COMMISSIONER OF CENTRAL EXCISE, KANPUR 295

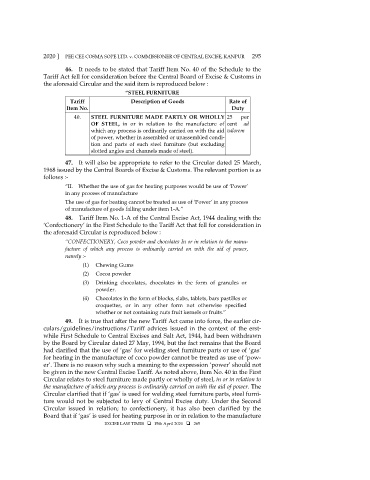

46. It needs to be stated that Tariff Item No. 40 of the Schedule to the

Tariff Act fell for consideration before the Central Board of Excise & Customs in

the aforesaid Circular and the said item is reproduced below :

“STEEL FURNITURE

Tariff Description of Goods Rate of

Item No. Duty

40. STEEL FURNITURE MADE PARTLY OR WHOLLY 25 per

OF STEEL, in or in relation to the manufacture of cent ad

which any process is ordinarily carried on with the aid valorem

of power, whether in assembled or unassembled condi-

tion and parts of such steel furniture (but excluding

slotted angles and channels made of steel).

47. It will also be appropriate to refer to the Circular dated 25 March,

1968 issued by the Central Boards of Excise & Customs. The relevant portion is as

follows :-

“II. Whether the use of gas for heating purposes would be use of ‘Power’

in any process of manufacture

The use of gas for heating cannot be treated as use of ‘Power’ in any process

of manufacture of goods falling under item 1-A.”

48. Tariff Item No. 1-A of the Central Excise Act, 1944 dealing with the

‘Confectionery’ in the First Schedule to the Tariff Act that fell for consideration in

the aforesaid Circular is reproduced below :

“CONFECTIONERY, Coco powder and chocolates In or in relation to the manu-

facture of which any process is ordinarily carried on with the aid of power,

namely :-

(1) Chewing Gums

(2) Cocoa powder

(3) Drinking chocolates, chocolates in the form of granules or

powder.

(4) Chocolates in the form of blocks, slabs, tablets, bars pastilles or

croquettes, or in any other form not otherwise specified

whether or not containing nuts fruit kernels or fruits.”

49. It is true that after the new Tariff Act came into force, the earlier cir-

culars/guidelines/instructions/Tariff advices issued in the context of the erst-

while First Schedule to Central Excises and Salt Act, 1944, had been withdrawn

by the Board by Circular dated 27 May, 1994, but the fact remains that the Board

had clarified that the use of ‘gas’ for welding steel furniture parts or use of ‘gas’

for heating in the manufacture of coco powder cannot be treated as use of ‘pow-

er’. There is no reason why such a meaning to the expression ‘power’ should not

be given in the new Central Excise Tariff. As noted above, Item No. 40 in the First

Circular relates to steel furniture made partly or wholly of steel, in or in relation to

the manufacture of which any process is ordinarily carried on with the aid of power. The

Circular clarified that if ‘gas’ is used for welding steel furniture parts, steel furni-

ture would not be subjected to levy of Central Excise duty. Under the Second

Circular issued in relation; to confectionery, it has also been clarified by the

Board that if ‘gas’ is used for heating purpose in or in relation to the manufacture

EXCISE LAW TIMES 15th April 2020 265