Page 156 - GSTL_26th March 2020_Vol 34_Part 4

P. 156

666 GST LAW TIMES [ Vol. 34

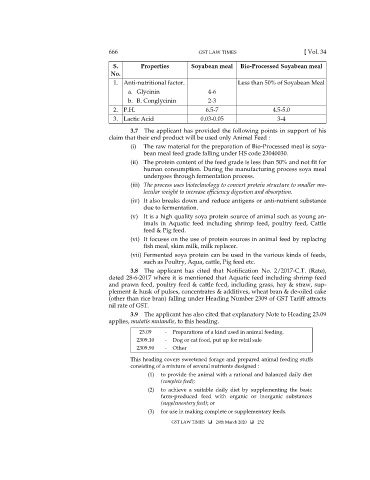

S. Properties Soyabean meal Bio-Processed Soyabean meal

No.

1. Anti-nutritional factor. Less than 50% of Soyabean Meal

a. Glycinin 4-6

b. B. Conglycinin 2-3

2. P.H. 6.5-7 4.5-5.0

3. Lactic Acid 0.03-0.05 3-4

3.7 The applicant has provided the following points in support of his

claim that their end product will be used only Animal Feed :

(i) The raw material for the preparation of Bio-Processed meal is soya-

bean meal feed grade falling under HS code 23040030.

(ii) The protein content of the feed grade is less than 50% and not fit for

human consumption. During the manufacturing process soya meal

undergoes through fermentation process.

(iii) The process uses biotechnology to convert protein structure to smaller mo-

lecular weight to increase efficiency digestion and absorption.

(iv) It also breaks down and reduce antigens or anti-nutrient substance

due to fermentation.

(v) It is a high quality soya protein source of animal such as young an-

imals in Aquatic feed including shrimp feed, poultry feed, Cattle

feed & Pig feed.

(vi) It focuses on the use of protein sources in animal feed by replacing

fish meal, skim milk, milk replacer.

(vii) Fermented soya protein can be used in the various kinds of feeds,

such as Poultry, Aqua, cattle, Pig feed etc.

3.8 The applicant has cited that Notification No. 2/2017-C.T. (Rate),

dated 28-6-2017 where it is mentioned that Aquatic feed including shrimp feed

and prawn feed, poultry feed & cattle feed, including grass, hay & straw, sup-

plement & husk of pulses, concentrates & additives, wheat bran & de-oiled cake

(other than rice bran) falling under Heading Number 2309 of GST Tariff attracts

nil rate of GST.

3.9 The applicant has also cited that explanatory Note to Heading 23.09

applies, mutatis mutandis, to this heading.

23.09 - Preparations of a kind used in animal feeding.

2309.10 - Dog or cat food, put up for retail sale

2309.90 - Other

This heading covers sweetened forage and prepared animal feeding stuffs

consisting of a mixture of several nutrients designed :

(1) to provide the animal with a rational and balanced daily diet

(complete feed);

(2) to achieve a suitable daily diet by supplementing the basic

farm-produced feed with organic or inorganic substances

(supplementary feed); or

(3) for use in making complete or supplementary feeds.

GST LAW TIMES 26th March 2020 252