Page 159 - GSTL_26th March 2020_Vol 34_Part 4

P. 159

2020 ] IN RE : VIPPY INDUSTRIES LTD. 669

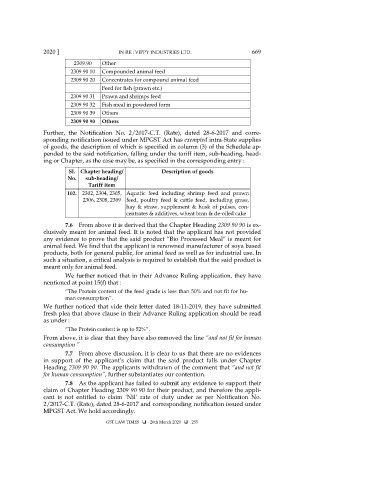

2309.90 Other

2309 90 10 Compounded animal feed

2309 90 20 Concentrates for compound animal feed

Feed for fish (prawn etc.)

2309 90 31 Prawn and shrimps feed

2309 90 32 Fish meal in powdered form

2309 90 39 Others

2309 90 90 Others

Further, the Notification No. 2/2017-C.T. (Rate), dated 28-6-2017 and corre-

sponding notification issued under MPGST Act has exempted intra-State supplies

of goods, the description of which is specified in column (3) of the Schedule ap-

pended to the said notification, falling under the tariff item, sub-heading, head-

ing or Chapter, as the case may be, as specified in the corresponding entry :

Sl. Chapter heading/ Description of goods

No. sub-heading/

Tariff item

102. 2302, 2304, 2305, Aquatic feed including shrimp feed and prawn

2306, 2308, 2309 feed, poultry feed & cattle feed, including grass,

hay & straw, supplement & husk of pulses, con-

centrates & additives, wheat bran & de-oiled cake

7.6 From above it is derived that the Chapter Heading 2309 90 90 is ex-

clusively meant for animal feed. It is noted that the applicant has not provided

any evidence to prove that the said product “Bio Processed Meal” is meant for

animal feed. We find that the applicant is renowned manufacturer of soya based

products, both for general public, for animal feed as well as for industrial use. In

such a situation, a critical analysis is required to establish that the said product is

meant only for animal feed.

We further noticed that in their Advance Ruling application, they have

nentioned at point 15(f) that :

“The Protein content of the feed grade is less than 50% and not fit for hu-

man consumption”.

We further noticed that vide their letter dated 18-11-2019, they have submitted

fresh plea that above clause in their Advance Ruling application should be read

as under :

“The Protein content is up to 52%”.

From above, it is clear that they have also removed the line “and not fit for human

consumption ”

7.7 From above discussion, it is clear to us that there are no evidences

in support of the applicant’s claim that the said product falls under Chapter

Heading 2309 90 90. The applicants withdrawn of the comment that “and not fit

for human consumption”, further substantiates our contention.

7.8 As the applicant has failed to submit any evidence to support their

claim of Chapter Heading 2309 90 90 for their product, and therefore the appli-

cant is not entitled to claim ‘Nil’ rate of duty under as per Notification No.

2/2017-C.T. (Rate), dated 28-6-2017 and corresponding notification issued under

MPGST Act. We hold accordingly.

GST LAW TIMES 26th March 2020 255