Page 129 - GSTL_23rd July 2020_Vol 38_Part 4

P. 129

2020 ] IN RE : A.B. ENTERPRISE 495

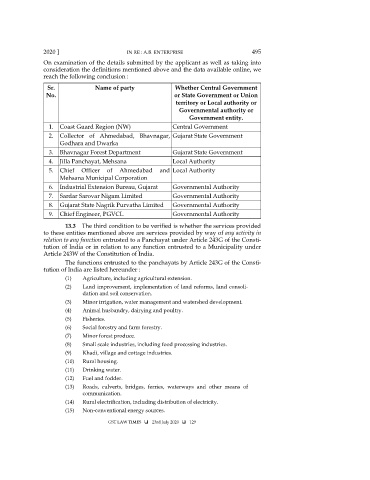

On examination of the details submitted by the applicant as well as taking into

consideration the definitions mentioned above and the data available online, we

reach the following conclusion :

Sr. Name of party Whether Central Government

No. or State Government or Union

territory or Local authority or

Governmental authority or

Government entity.

1. Coast Guard Region (NW) Central Government

2. Collector of Ahmedabad, Bhavnagar, Gujarat State Government

Godhara and Dwarka

3. Bhavnagar Forest Department Gujarat State Government

4. Jilla Panchayat, Mehsana Local Authority

5. Chief Officer of Ahmedabad and Local Authority

Mehsana Municipal Corporation

6. Industrial Extension Bureau, Gujarat Governmental Authority

7. Sardar Sarovar Nigam Limited Governmental Authority

8. Gujarat State Nagrik Purvatha Limited Governmental Authority

9. Chief Engineer, PGVCL Governmental Authority

13.3 The third condition to be verified is whether the services provided

to these entities mentioned above are services provided by way of any activity in

relation to any function entrusted to a Panchayat under Article 243G of the Consti-

tution of India or in relation to any function entrusted to a Municipality under

Article 243W of the Constitution of India.

The functions entrusted to the panchayats by Article 243G of the Consti-

tution of India are listed hereunder :

(1) Agriculture, including agricultural extension.

(2) Land improvement, implementation of land reforms, land consoli-

dation and soil conservation.

(3) Minor irrigation, water management and watershed development.

(4) Animal husbandry, dairying and poultry.

(5) Fisheries.

(6) Social forestry and farm forestry.

(7) Minor forest produce.

(8) Small scale industries, including food processing industries.

(9) Khadi, village and cottage industries.

(10) Rural housing.

(11) Drinking water.

(12) Fuel and fodder.

(13) Roads, culverts, bridges, ferries, waterways and other means of

communication.

(14) Rural electrification, including distribution of electricity.

(15) Non-conventional energy sources.

GST LAW TIMES 23rd July 2020 129