Page 114 - GSTL_27th August 2020_Vol 39_Part 4

P. 114

440 GST LAW TIMES [ Vol. 39

of Exempted Goods as per Sr. No. 102 of Notification No. 2/2017-

Central Tax (Rate), dated 28-6-2017 is correct or not?

(B) Whether the goods falling under TSH 2309 90 10 of Customs Tariff

Act, 1975 as adopted to GST can be treated as ‘waste of sugar manu-

facture, whether or not in the form of pellets under Heading 2303’

attracting 5% of IGST (2.5% CGST + 2.5% SGST) as per Schedule-I

(Sr. No. 104) of Notification No. 1/2017-C.T. (Rate), dated 28-6-2017

or not?

At the outset, we would like to make it clear that the provisions of both the CGST

Act and the MGST Act are the same except for certain provisions. Therefore, un-

less a mention is specifically made to any dissimilar provisions, a reference to the

CGST Act would also mean a reference to the same provision under the MGST

Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, a

reference to “GST Act” would mean CGST Act and MGST Act.

2. Facts and contention - As per the applicant :

The submissions made by the applicant is as under :-

2.1 M/s. Madhurya Chemical (hereinafter referred as ‘applicant’) is en-

gaged in supply of ‘Shatamrut Chyavan’ (hereinafter referred to, as the subject

product) which is a complete animal feed supplement and is used as a supple-

mentary product to increase the nutritional value of molasses. In other words, it

is a nutrition supplement to the cattle feed but cannot be treated as cattle feed in

isolation.

2.2 The applicant has furnished a detailed plant drawing cum-flow

chart of the manufacturing process to understand how the subject product is

produced out of sugarcane molasses and has stated that to manufacture the

product, other than molasses, 15 other ingredients are also mixed in the molasses

(input) to increase the nutrition value of the molasses.

2.3 Applicant has classified the subject product, till the date of applica-

tion, under Chapter 2309 90 10, attracting ‘NIL’ rate of GST.

2.4 Notification No. 2/2017-C.T. (Rate), dated 28-6-2017, as amended,

specifies GST rate schedules and classification of subject product under Schedule.

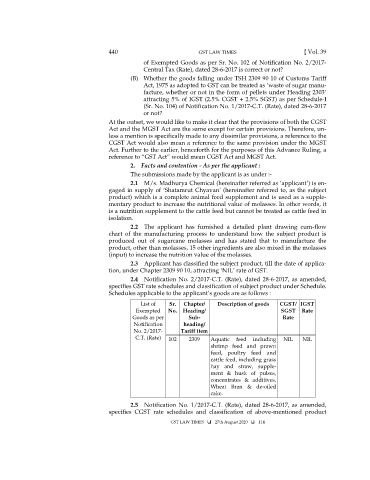

Schedules applicable to the applicant’s goods are as follows :

List of Sr. Chapter/ Description of goods CGST/ IGST

Exempted No. Heading/ SGST Rate

Goods as per Sub- Rate

Notification heading/

No. 2/2017- Tariff item

C.T. (Rate) 102 2309 Aquatic feed including NIL NIL

shrimp feed and prawn

feed, poultry feed and

cattle feed, including grass

hay and straw, supple-

ment & husk of pulses,

concentrates & additives,

Wheat Bran & de-oiled

cake.

2.5 Notification No. 1/2017-C.T. (Rate), dated 28-6-2017, as amended,

specifies CGST rate schedules and classification of above-mentioned product

GST LAW TIMES 27th August 2020 114