Page 115 - GSTL_27th August 2020_Vol 39_Part 4

P. 115

2020 ] IN RE : VIVEK V. RATNAPARKHI 441

under Schedule. The Schedule applicable to the subject product as per the ‘speci-

fication of product’ is as follows :

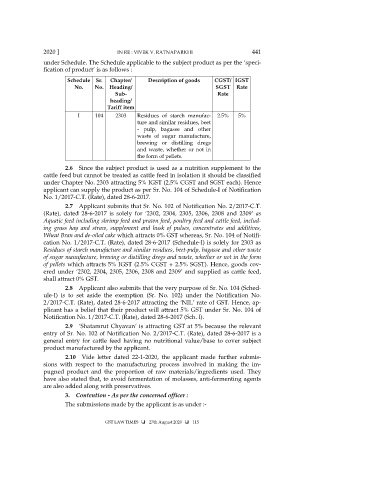

Schedule Sr. Chapter/ Description of goods CGST/ IGST

No. No. Heading/ SGST Rate

Sub- Rate

heading/

Tariff item

I 104 2303 Residues of starch manufac- 2.5% 5%

ture and similar residues, beet

- pulp, bagasse and other

waste of sugar manufacture,

brewing or distilling dregs

and waste, whether or not in

the form of pellets.

2.6 Since the subject product is used as a nutrition supplement to the

cattle feed but cannot be treated as cattle feed in isolation it should be classified

under Chapter No. 2303 attracting 5% IGST (2.5% CGST and SGST each). Hence

applicant can supply the product as per Sr. No. 104 of Schedule-I of Notification

No. 1/2017-C.T. (Rate), dated 28-6-2017.

2.7 Applicant submits that Sr. No. 102 of Notification No. 2/2017-C.T.

(Rate), dated 28-6-2017 is solely for ‘2302, 2304, 2305, 2306, 2308 and 2309’ as

Aquatic feed including shrimp feed and prawn feed, poultry feed and cattle feed, includ-

ing grass hay and straw, supplement and husk of pulses, concentrates and additives,

Wheat Bran and de-oiled cake which attracts 0% GST whereas, Sr. No. 104 of Notifi-

cation No. 1/2017-C.T. (Rate), dated 28-6-2017 (Schedule-I) is solely for 2303 as

Residues of starch manufacture and similar residues, beet-pulp, bagasse and other waste

of sugar manufacture, brewing or distilling dregs and waste, whether or not in the form

of pellets which attracts 5% IGST (2.5% CGST + 2.5% SGST). Hence, goods cov-

ered under ‘2302, 2304, 2305, 2306, 2308 and 2309’ and supplied as cattle feed,

shall attract 0% GST.

2.8 Applicant also submits that the very purpose of Sr. No. 104 (Sched-

ule-I) is to set aside the exemption (Sr. No. 102) under the Notification No.

2/2017-C.T. (Rate), dated 28-6-2017 attracting the ‘NIL’ rate of GST. Hence, ap-

plicant has a belief that their product will attract 5% GST under Sr. No. 104 of

Notification No. 1/2017-C.T. (Rate), dated 28-6-2017 (Sch. I).

2.9 ‘Shatamrut Chyavan’ is attracting GST at 5% because the relevant

entry of Sr. No. 102 of Notification No. 2/2017-C.T. (Rate), dated 28-6-2017 is a

general entry for cattle feed having no nutritional value/base to cover subject

product manufactured by the applicant.

2.10 Vide letter dated 22-1-2020, the applicant made further submis-

sions with respect to the manufacturing process involved in making the im-

pugned product and the proportion of raw materials/ingredients used. They

have also stated that, to avoid fermentation of molasses, anti-fermenting agents

are also added along with preservatives.

3. Contention - As per the concerned officer :

The submissions made by the applicant is as under :-

GST LAW TIMES 27th August 2020 115