Page 54 - GSTL_7th May 2020_Vol 36_Part 1

P. 54

12 GST LAW TIMES [ Vol. 36

sential Medicines’ means the National List of Essential Medicines, 2011 pub-

lished by the Ministry of Health and Family Welfare as updated and revised

from time to time. It also specifies that the National List of Essential Medicines,

2011 is included in the First Schedule to the order. Para 2(2) stipulates that all

other words and expressions used therein and not defined, but defined in the

1940 Act shall have meanings respectively assigned in the 1940 Act.

23. The First Schedule contains the National List of Essential Medicines,

2011. The relevant portion is extracted below :

“Schedule-I

(See paragraphs - 2(t), 2(zb))

Symbols P, S and T appearing in NLEM, 2011 denote essentially at Primary,

Secondary and Tertiary levels respectively.

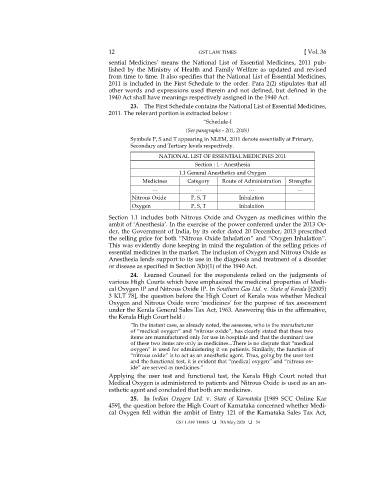

NATIONAL LIST OF ESSENTIAL MEDICINES 2011

Section : 1 - Anesthesia

1.1 General Anesthetics and Oxygen

Medicines Category Route of Administration Strengths

… … … …

Nitrous Oxide P, S, T Inhalation

Oxygen P, S, T Inhalation

Section 1.1 includes both Nitrous Oxide and Oxygen as medicines within the

ambit of ‘Anesthesia’. In the exercise of the power conferred under the 2013 Or-

der, the Government of India, by its order dated 20 December, 2013 prescribed

the selling price for both “Nitrous Oxide Inhalation” and “Oxygen Inhalation”.

This was evidently done keeping in mind the regulation of the selling prices of

essential medicines in the market. The inclusion of Oxygen and Nitrous Oxide as

Anesthesia lends support to its use in the diagnosis and treatment of a disorder

or disease as specified in Section 3(b)(1) of the 1940 Act.

24. Learned Counsel for the respondents relied on the judgments of

various High Courts which have emphasized the medicinal properties of Medi-

cal Oxygen IP and Nitrous Oxide IP. In Southern Gas Ltd. v. State of Kerala [(2005)

3 KLT 78], the question before the High Court of Kerala was whether Medical

Oxygen and Nitrous Oxide were ‘medicines’ for the purpose of tax assessment

under the Kerala General Sales Tax Act, 1963. Answering this in the affirmative,

the Kerala High Court held :

“In the instant case, as already noted, the assessee, who is the manufacturer

of “medical oxygen” and “nitrous oxide”, has clearly stated that these two

items are manufactured only for use in hospitals and that the dominant use

of these two items are only as medicines...There is no dispute that “medical

oxygen” is used for administering it on patients. Similarly, the function of

“nitrous oxide” is to act as an anesthetic agent. Thus, going by the user test

and the functional test, it is evident that “medical oxygen” and “nitrous ox-

ide” are served as medicines.”

Applying the user test and functional test, the Kerala High Court noted that

Medical Oxygen is administered to patients and Nitrous Oxide is used as an an-

esthetic agent and concluded that both are medicines.

25. In Indian Oxygen Ltd. v. State of Karnataka [1989 SCC Online Kar

459], the question before the High Court of Karnataka concerned whether Medi-

cal Oxygen fell within the ambit of Entry 121 of the Karnataka Sales Tax Act,

GST LAW TIMES 7th May 2020 54