Page 121 - GSTL_14th May 2020_Vol 36_Part 2

P. 121

2020 ] IN RE : GURUKRUPA HOSPITALITY SERVICES 223

4.3 It is further opined by the Commissionerate that as per classifica-

tion of services provided vide Notification No. 11/2017-C.T. (Rate), dated 28-6-

2017, the activity carried out by the applicant appears to be in the nature of ser-

vice provided in canteen and other similar establishments and also classifiable

under Chapter Heading 9963 33 and GST @ rate of 18% is applicable on that ser-

vice. It is further submitted that the question raised by the applicant in the au-

thority of advance ruling is not covered in the category of advance ruling as the

category of service is very much clear in the Chapter Note 9963 33.

5. Now, we discuss the issue in two parts viz. taxability of subject sup-

ply of services up to 25-7-2018 and w.e.f. 26-7-2018, due to amendments in subject

Notifications, as below :

A. Taxabilty up to 25-7-2018 :

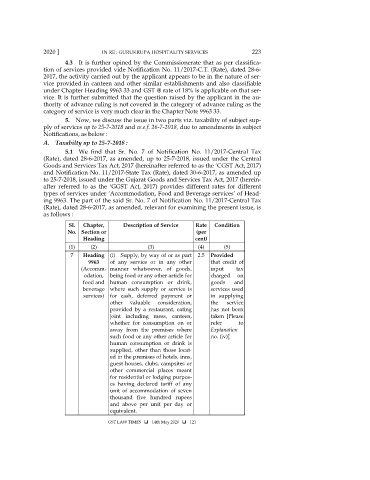

5.1 We find that Sr. No. 7 of Notification No. 11/2017-Central Tax

(Rate), dated 28-6-2017, as amended, up to 25-7-2018, issued under the Central

Goods and Services Tax Act, 2017 (hereinafter referred to as the ‘CGST Act, 2017)

and Notification No. 11/2017-State Tax (Rate), dated 30-6-2017, as amended up

to 25-7-2018, issued under the Gujarat Goods and Services Tax Act, 2017 (herein-

after referred to as the ‘GGST Act, 2017) provides different rates for different

types of services under ‘Accommodation, Food and Beverage services’ of Head-

ing 9963. The part of the said Sr. No. 7 of Notification No. 11/2017-Central Tax

(Rate), dated 28-6-2017, as amended, relevant for examining the present issue, is

as follows :

Sl. Chapter, Description of Service Rate Condition

No. Section or (per

Heading cent)

(1) (2) (3) (4) (5)

7 Heading (i) Supply, by way of or as part 2.5 Provided

9963 of any service or in any other that credit of

(Accomm- manner whatsoever, of goods, input tax

odation, being food or any other article for charged on

food and human consumption or drink, goods and

beverage where such supply or service is services used

services) for cash, deferred payment or in supplying

other valuable consideration, the service

provided by a restaurant, eating has not been

joint including mess, canteen, taken [Please

whether for consumption on or refer to

away from the premises where Explanation

such food or any other article for no. (iv)]

human consumption or drink is

supplied, other than those locat-

ed in the premises of hotels, inns,

guest houses, clubs, campsites or

other commercial places meant

for residential or lodging purpos-

es having declared tariff of any

unit of accommodation of seven

thousand five hundred rupees

and above per unit per day or

equivalent.

GST LAW TIMES 14th May 2020 121